Young firms often seek growth capital to expand operations, and of those that choose to pursue an IPO, roughly 2/3 have raised capital from venture capitalists (VCs). The 2/3 proportion varies by year and is greater when lots of tech firms are in the markets (e.g., the dot-com era). In my research paper with Dr. Colette Southam published in Venture Capital journal, we find that a VC-backed firm is 14% more likely to fail to complete its IPO. Not all “failures” are bad; some firms instead accepted buyout bids. Nevertheless, why do VC-backed firms “fail”? In the research we find two primary reasons. First, VC-backed firms have an alternative to a low IPO price. Instead, the VC can fund another round and then retry the IPO later. Second, VC-backers more often “test the waters” of the IPO markets with firms that are too risky or too early and are screened out by astute equity investors. Does this mean your firm should avoid VC-backing? Quite the contrary, only a very tiny proportion of private firms raise VC money, while most firms going public have VC-backing. VC backing increases your chances of ever getting to the IPO stage.

Author Archives: Kevin

When IPOs fail, competitors benefit

A firm seeking to go public in the U.S. files documents with the SEC. With some minor limitations, it can withdraw from the process at any time. Understandably, media focus is on IPO successes rather than failures, although more than one in five filers does so. Withdrawal is not always a bad thing. For some firms a better offer arrives (e.g., a buyout bid) while for others it is a bad thing (e.g., investors are unwilling to invest). Importantly, the net result of a withdrawal is one less publicly traded competitor. In a recent paper I have with Dr. Craig Dunbar, we show that the existing publicly traded competitors experience a positive cumulative abnormal return of about .35% when a “would be” competitor fails to complete its IPO. Can you profit from this? Not likely. You would have to predict a withdrawal, and then buy stock in competing firms. Only those inside the firm’s IPO process would have enough insight. The rest of us must read the tea leaves.

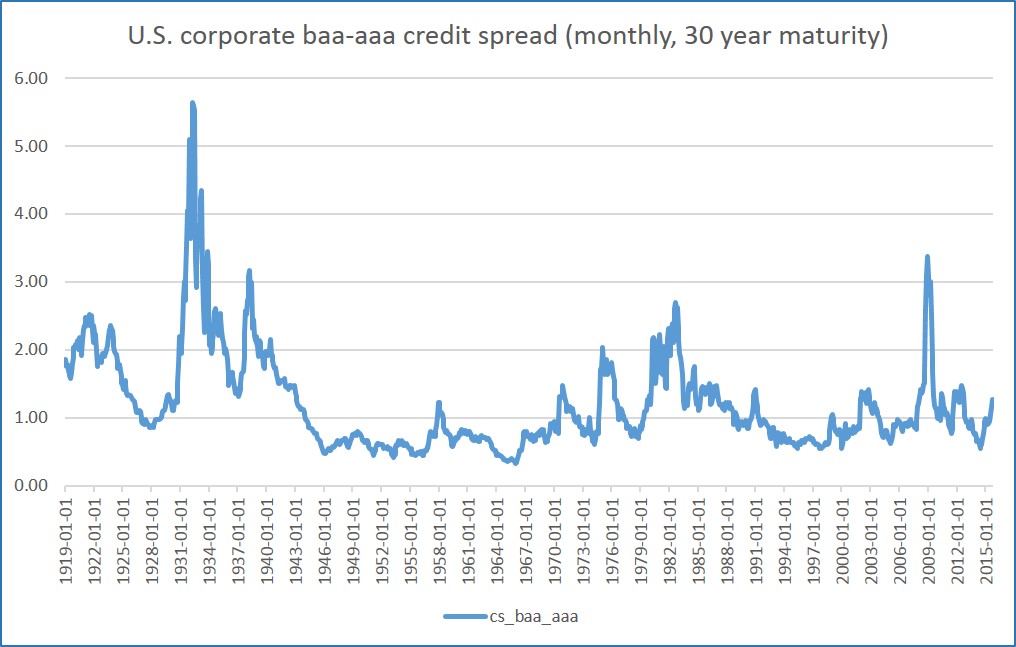

The graph shows the monthly U.S. corporate credit spread of Baa-rated bonds minus AAA-rated bonds. The bond yields are calculated as Moody’s seasoned corporate bond yields with maturities as close as possible to 30 years. Meaning? When the likelihood of default increases, the bond yield increases. Baa firms are more likely to default than AAA firms. When good economic conditions are expected, investors expect both Baa and AAA firms not to default, and thus the credit spread is small. When poor economic conditions are expected, the likelihood of default of all firms increases, more so for Baa firms. As such, investors demand greater return (yield) and so we see the credit spread increase. A high spread generally indicates(expected) poor economic conditions.

A data file is here.

Withdrawn IPOs are far more common that most people think. Using a set of screens to reduce the universe of typical IPOs studied in the finance field, just over a third of intended IPO-seeking firms withdraw their filings and pursue other paths. The data below show the volume of withdrawn IPOs by year from 1998-2013. This is an incredibly important (and understudied) topic.

In research we apply various screens to the universe of IPOs, and study a subset of “clean” IPOs. We commonly screen IPOs that have unique pricing processes, legal/ownership structures, disclosure requirements, or are small offerings/firms. The data below use typical screens showing the volume of completed U.S. IPOs. Note: a deal can be screen for more than one reason.

What is a good strategy?

A good strategy is one you would not be stupid not to do. What does that mean? In part, that means that it is not necessarily obvious. Similarly, good (business) innovations are generally novel but also uncertain before becoming reality. Good strategies share must also be novel and not obvious because if they were obvious someone else would likely would have already done it. They are uncertain because the likelihood of successful execution is unclear — if it were certain, someone would have done it, right? Imagine a spectrum of strategies from “stupid” to “brilliant”. The stupid ideas are bad, while the brilliant ideas have already been done suggesting that good strategies fall somewhere in between. Using this novelty-uncertainty framework, a good strategy will be developed and implemented only when you have people capable of novel/disruptive thought, but also willing to tolerate uncertainty, (one would hope) driven by their confidence in their ability to execute.

Chrysler IPO…Fail?

Chrysler Group LLC has withdrawn its planned IPO. See the filing here. Earlier this year I posted about firms that file for their IPO as a mechanism to attract M&A bids. This is a similar example. Instead of completing the IPO, Chrysler scrapped it after Fiat agreed to buy the ownership stake that was to be sold in the IPO. Fiat bought ~41.46% of Chrysler owned by the union. The stake had been for sale (to Fiat, among other buyers) but the groups could not agree on a valuation. The IPO filing created a credible threat that forced Fiat’s hand, but also served as a price discovery process and allowed both sides to better realize a fair market value for the stake. A properly orchestrated IPO can serve several purposes.

How to rebound from a failed IPO

Despite going through the time-consuming IPO process, roughly 1 in 3 would-be issuers fails to complete its IPO and instead withdraws. Not all withdrawals are bad, and in fact some firms instead (e.g.) accept a buyout bid while others simply return to private status and raise no more money. In a paper with Dr. Craig Dunbar, we study the determinants of the success of firms that “fail” IPOs. Firms with venture capital backing or prestigious investment bankers are 24% and 8% (respectively) more likely to rebound from a failed IPO to conduct a private placement, merger/acquisition, or to re-file and complete an IPO. As well, firms with more underwriters on their IPO and with more revenue obtain better valuations in those post-withdrawal events. The former occurs because the underwriters compete to advise the withdrawn firm on its subsequent deal. Firms considering the IPO path and want a stronger fallback position should generally wait until revenues are strong, obtain venture capital backing, hire a prestigious investment bank, and ensure there are enough underwriters involved to foster a healthy competition for their business. Once gain, competition works!

Facebook IPO versus the S&P500

Facebook (NASD: FB) issued its IPO at $38 and began trading May 18, 2012. Atypical of IPOs it immediately fell and then closed as low as $17.73 (53% loss) on September 4, 2012, remaining below its IPO price until August 2, 2013. On January 12, 2014 it closed at $57.94, a 52% gain. While many called this a botched IPO, the underwriters did well by the issuer by not leaving money “on the table” as happens when an IPO runs up after issuance. Was this a good investment for IPO investors? Since the issuance, FB has returned 52% while the S&P500 has returned 46%. On an annualized basis those returns are 29% and 26% respectively. So, FB wins, right? Hardly. Owners of FB have suffered extreme volatility — they woke up each day wondering whether they were richer or poorer. Investors dislike uncertainty, and so must typically be compensated for enduring it. Because FB has not been public long enough to reliably calculate a beta (a typical measure of relative uncertainty), we can instead compare the returns as adjusted by their respective standard deviations (Sharpe ratios from Nobel laureate, William F. Sharpe). The annualized standard deviation of FB and the S&P500 since the IPO have been around 54% and 12%. Using the annualized excess returns of FB and S&P500 plus the risk measure above, the Sharpe ratios have been 0.54 and 2.15 (higher is better). Holding the S&P500 was a far better risk-adjusted return investment for investors.

Bad governance linked to IPO failure

Does your board of directors matter when conducting an IPO? In a research paper (pdf) published with Dr. Colette Southam, we study the governance structure of over 1600 IPOs to determine the effects on IPO failure. We find three interesting effects. First, when the CEO and Chair (of the board) are separated, a deal is 4% less likely to fail. Investors prefer the added oversight of having these roles separated. We also find two important board characteristics that a firm can change before the IPO. As it turns out, the size of the board does NOT affect whether the IPO is completed, but having experienced board members makes the firm less likely to fail. Investors in the market examine the governance structure and consider it when deciding whether to invest in an IPO. If you are considering an IPO, it pays to separate your CEO and Chair roles, and to build a board of seasoned executives…simply adding more board members does not matter.